After a decade of being trounced by Tesla Inc., this was supposed to be the year that traditional automakers finally put up a fight for electric cars. General Motors was committing its biggest brands to a new line of electric models; Ford and Volkswagen were ramping up production of EVs designed for the masses. It was, many predicted, time for the automotive world order to re-assert itself.

Things haven’t turned out that way. Ford’s vaunted F-150 Lightning has been outsold by the R1T from Rivian, a startup that sold its first vehicle just two years ago. GM’s lineup of new EVs has suffered crippling setbacks in battery manufacturing. In July, Volkswagen Chief Executive Officer Thomas Schaefer succinctly summarized his own company’s EV competitiveness: “The roof is on fire.”

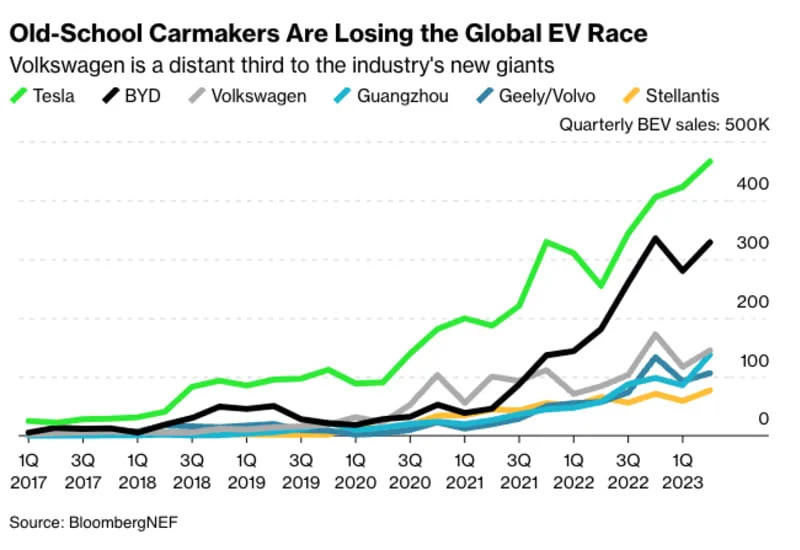

With just three months remaining, 2023 has been less a redemption story for legacy automakers than further evidence of their quagmire. In the US, Tesla has been expanding production about as fast as all of its competitors combined. The Austin, Texas-based EV maker accounts for 61% of fully electric cars ever sold in the US, making it more dominant in EVs than Apple is in smartphones.

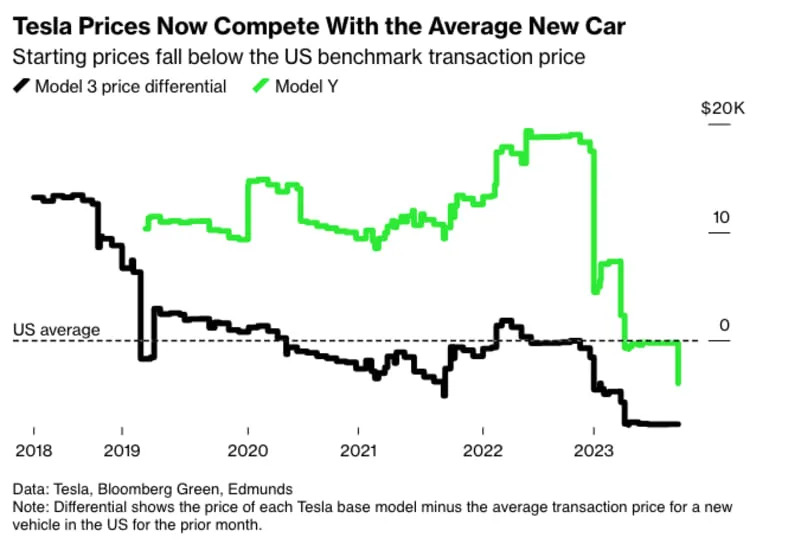

No one can keep up with Tesla’s price cuts

Tesla started the year with a dramatic salvo of price cuts that reset customer expectations across the industry. Before the changes, the cheapest version of Tesla’s Model Y SUV cost nearly $20,000 more than the average selling price of a new car in the US. By April, that differential had evaporated.

The latest shot fired in Tesla’s price war came on Oct. 1, when it introduced a new Model Y variant that starts at $4,000 less than the average selling price of a new vehicle in the US. The Model Y is on track to be the best-selling car in the world for 2023 — even after the price cuts, it’s doing so with higher profit margins than most automakers make on their gasoline vehicles.

Ford was first to respond with dramatic price cuts of it its own. But even a reduction of up to $10,000 for the F-150 Lightning wasn’t enough to keep Ford’s EV expansion plans on schedule. By July, CEO Jim Farley throttled back production targets through 2026, saying the company expects to lose about $4.5 billion on EVs this year. “The pricing pressure has increased dramatically,” Farley said.

GM, the biggest US automaker by vehicle sales, is also spinning its wheels. The company’s hopes are pinned to new batteries made by its Ultium LLC joint venture with Korea’s LG Energy Solution, which are expected to reduce costs. But delays have put in limbo the availability of GM’s new electric Chevy Blazer, Equinox and Silverado.

Ford, GM and Stellantis, meanwhile, are now locked in contract negotiations with the United Auto Workers union, which may lead to higher labor costs during the cash-torching catch-up phase of the EV transition. (Stellantis doesn’t plan to make its first electric Ram trucks and Wrangler Jeeps until the end of next year.)

Tesla’s only real competitor

There’s only one company that competes at Tesla’s scale on electric vehicles: China’s BYD. It’s also the first example of an incumbent that successfully transitioned from selling gas-powered cars to profitable electric vehicles.

BYD’s history is itself unique. The company started off as a battery manufacturer, making tiny power packs for Nokia cell phones and Dell laptop computers in the 1990s. When it moved into autos in the 21st century, it did so with a battery-maker’s mindset. In 2009, while Tesla was gluing together batteries in Silicon Valley for its electric Roadsters, BYD was building electric buses in Hunan Province.

Core to the problem for the incumbents is how they’ve largely become assemblers of third-party components. It was easy to assume that just as transmissions and infotainment systems could be outsourced, so could the building blocks for EVs — batteries, motors, software, charging infrastructure. But that hasn’t been a winning strategy.

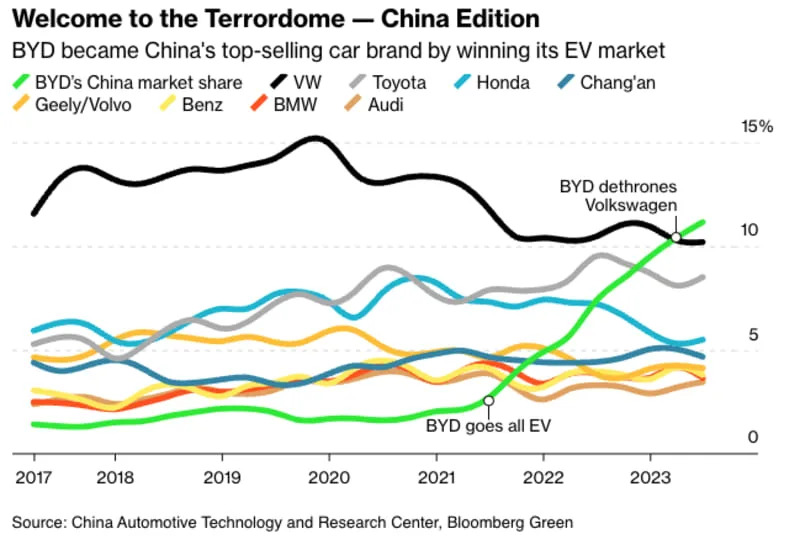

BYD didn’t become a dominant automaker in China until it decided in 2021 to stop making cars without plugs. The decision allowed the company to focus entirely on EVs and what was needed for their success. Within two years it dethroned Volkswagen as the best-selling car brand in China; in the third quarter of this year, BYD came within a whisker of delivering more fully electric vehicles globally than even Tesla.

BYD’s dramatic rise shows that it’s possible for a traditional automaker to go electric, but it may require excising the very products and business practices that once made them successful. Few others have committed to doing the same — even within a 10-year timeframe.

The truck wars are coming

Tesla started this consequential year in EVs with a bang, and it may end it with another. Two years behind schedule, the company is expected to finally start selling its first electric pickup, the Cybertruck, in coming weeks. A launch date hasn’t been announced.

The truck is an alien-looking mass of stainless steel and glass — the most radical departure in both form and function that the pickup world has seen in generations. And while many in the industry have laughed it off, maybe they shouldn’t. Pricey pickups account for a fraction of US legacy auto sales but a majority of the industry’s profits. If trucks start to go electric as quickly as cars and SUVs have, then the electrification of the F-150, Silverado and Ram will be of existential importance to Ford, GM and Stellantis.

Things aren’t off to a great start. The F-150 Lightning is the furthest along, but after 18 months it amounts to just 3% of traditional F-Series sales. GM sold just 18 of its delayed Silverado EVs in their third-quarter debut, and the Ram 1500 REV is still at least a year away. Flourish or flop, the Cybertruck is something that could only have been conceived at a company wholly dedicated to EVs. It’s a swing for the fences, and the industry seems unprepared for the possibility that it connects.

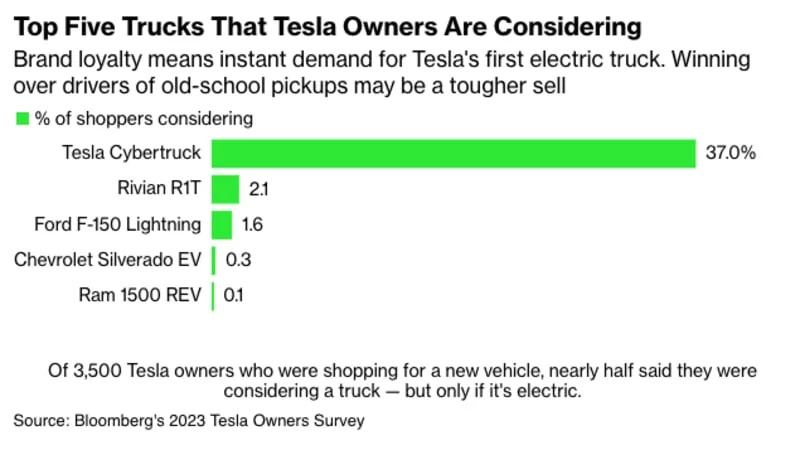

A Bloomberg survey of Tesla owners earlier this year found strong interest in pickups. Of 3,500 Tesla car owners who were in the market to buy another vehicle, 37% were considering a Cybertruck. The competition wasn’t close. About 2.1% of shoppers were looking at a Rivian, and that was more than the next three pickups combined. While the survey population might not represent the broader pickup market, it’s at least a sign of where EV shoppers are engaged.

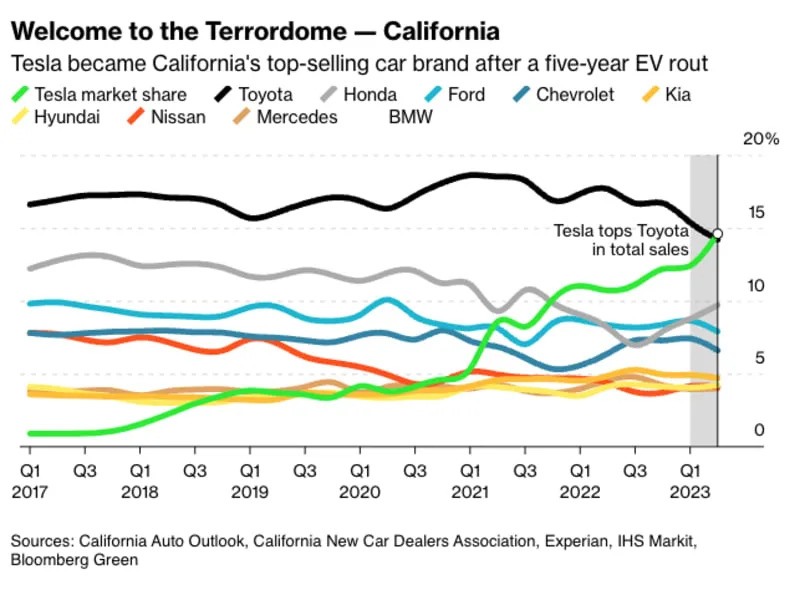

California presents a nightmare scenario

The transition to electric vehicles is looking less like an orderly adjustment to a new type of vehicle hardware than the sort of market-scrambling Yahtzee toss that allowed Apple to take over the smartphone industry. To see how it could play out from here, just look at California, which is roughly three or four years ahead of the US as a whole in terms of EV adoption. In that time, Tesla went from struggling startup to toppling Toyota as the best-selling car brand in America’s biggest auto market.

Tesla’s lead is hardly insurmountable. Next year large swaths of its proprietary charging network will open up to other automakers, which could double their availability of high-speed chargers and limit one of Tesla’s biggest advantages. Just since 2020, more than $100 billion has been invested in US EV and battery manufacturing, showing the vast resources being deployed on electrification.

It’s also still early. Tesla produces only a fraction of the cars bought by Americans — less than 5% of total sales so far in 2023. The assumption has always been that as EV adoption increases, incumbent automakers will mostly manage to regain their former places in the pecking order. Bank of America analysts estimated in June that Tesla’s share of the US EV market will drop to 18% by 2026.

But so far the gap isn’t closing, and the task gets harder as each year passes absent a breakout electric model. With scale comes manufacturing efficiency; with efficiency comes additional scale. It’s the same virtuous cycle that helped a handful of powerful automakers serve as constant gatekeepers to the car industry for the last century.

Read the full article here